On the economic roots of the covid event and probable near-term developments

On the sociology of deep politics pt. 2

Yes, this is an astonishing comment in light of the actual situation to be sure. Pinning that allegation on anti-lockdown protesters is a tad oxymoronic.

But there’s a more ominous theme here. They now explicitly blame protesters and political dissent for hampering economic activity and undermining people’s livelihoods:

Expect more of this theme in the near future.

The fact of the matter is that the world currently experiences a severe convergence of shortages and supply chain disruptions. Taken together, these are almost certainly unsolvable in the long run, meaning that global industrial civilization as we know it is not going to keep functioning for quite so many more years.

These disruptions are namely ultimately rooted in the structural energy crisis that’s commonly called peak oil (yeah, I know that there are people in these forums that reject this notion as just another authoritarian red herring - even Dave McGowan subscribed to the idea that the abiogenic synthesis of petroleum rendered the resource effectively inexhaustible - but let’s just say that I disagree here) which fans out across all other areas of the global economy due to the key role played by petroleum in every contemporary chain of production whatsoever, including your home-made cat wool sweaters unless your little darling subsists exclusively on foraging for wild pests.

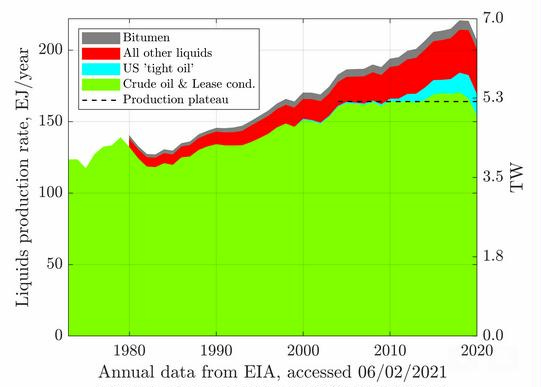

Here it is. That little top to the right. That’s total global petroleum production peaking in 2018. Conventional oil production plateaued in 2005 and peaked in 2008, at about the dotted line:

That’s not to say that petroleum shortages are the only resource bottleneck our globally interconnected civilization is currently up against, far from it. We’re low on lithium for all those supposedly forthcoming EVs, key rare earth minerals likewise, we’re short on the two core elements of synthetic fertilizer, phosphorous and synthetic nitrogen, and even copper is scarce, especially in relation to the predicted EV revolution. It sounds like a joke, but we’re actually also running low on sand suitable for concrete production. The list is quite long.

“I’ve been doing this 30 years and I’ve never seen markets like this,” Currie told Bloomberg TV in an interview on Monday. “This is a molecule crisis. We’re out of everything, I don’t care if it’s oil, gas, coal, copper, aluminum, you name it we’re out of it.”

(Goldman Sachs’ head commodity analyst Jeff Currie lamenting the unprecedented situation, Bloomberg Feb. 7, 2022)

Petroleum, however, is by far the most important resource in the modern economy, since it not only facilitates access to almost everything else, but also represents the most significant energy influx to the global economy considered as a complex system. Lots have been written on this issue, and Richard Heinberg’s books are probably the most accessible while also being quite informative. Tom Murphy’s Do the Math blog is also exceptionally clear and well-argued, and I’ve already mentioned Alice Friedemann and Gail Tverberg who are very much worth a read for those interested in digging a bit deeper.

Basically, the situation is that most of the cheap and easily extractable petroleum has already been exploited, leaving the global economy with a steady decrease in available net energy, since the actual energy expenditure necessary for the supply chains to retrieve and market the energy resources is increasing.

And while you can run an economy on a capital deficit for a while, you can’t run it on a real energy deficit.

This is nonetheless a very tough topic to digest for people who are more or less unfamiliar with it, and can easily lead to despondency since the facts of the matter so strongly conflict with core assumptions of the modern worldview. I don’t think that’s necessary, however, and would rather argue that the end and radical transformation of industrial society is to be welcomed by all of us, even if the process will be incredibly disruptive over generations.

And these disruptions are already on the horizon. Apart from the material scarcities already mentioned, the shortfall in petroleum production and current European energy crisis, the financial pressures are mounting.

So what does the financial situation have to do with energy resources, you may ask?

Well, one of the most significant aspects of the growth-based global capitalist economy is its effectiveness at basically offsetting shortages with the use of debt. This works brilliantly when it’s just a matter of redirecting resource flows, facilitating trade and moving stuff around on the board. In other words, the system is at least in principle effective at addressing relative scarcity, but when we’re dealing with the absolute scarcity of irreplaceable resources such as energy, then of course nothing really helps.

Yet what the world economy has been focusing on for at least the last 15 years, but arguably since the US crude oil production peak in the 70s, is precisely the attempt to offset a steadily lowering EROI (energy returned on energy invested) of the increasingly scarce, lower-quality and inaccessible petroleum resources by papering it over with debt. This works adequately well for a while, and can probably both mask the impact of the structural energy crisis as well as spread its consequences over larger sectors of the economy so as to prolong the process a bit.

But it can’t work forever. Indeed, the root cause of the “Great Recession” of 2007 and the subprime crisis that triggered this still reverberating event is found in unsustainable real energy costs brought about by actual scarcities. The much derided “financial shenanigans” and covert deregulation surrounding the events cannot just be reduced to amoral grifting, but must to some extent be considered an adaptive response by a system under severe strain. The attempt to balance resource flows and maintain nominal GDP growth using various forms of debt.

Since 2005, (1) world oil supply has not increased, and (2) the world has undergone its most severe economic crisis since the Depression. In this paper, logical arguments and direct evidence are presented suggesting that a reduction in oil supply can be expected to reduce the ability of economies to use debt for leverage. The expected impact of reduced oil supply combined with this reduced leverage is similar to the actual impact of the 2008–2009 recession in OECD countries. If world oil supply should continue to remain generally flat, there appears to be a significant possibility that oil consumption in OECD countries will continue to decline, as emerging markets consume a greater share of the total oil that is available. If this should happen, based on these findings we can expect a continuing financial crisis similar to the 2008–2009 recession including significant debt defaults (Tverberg, Gail, “Oil Supply Limits and the Continuing Financial Crisis”, Energy, vol. 37, issue 1, Jan. 2012)

And what we saw just prior to the covid event of early 2020 was precisely an incipient financial collapse related to US government debt, i.e. the treasuries market. In September of 2019, the interest rates on overnight repos, short-term loans between major financial institutions, spiked, triggering a still ongoing systemic bailout similar to the QE interventions we saw in the aftermath of the 2007 crisis.

Such a bailout was inevitable. A lack of liquidity in the repo market would freeze capital flows everywhere, since this is where financial institutions go for short-term credit. Everything would have ground to a halt without the more than $9 trillion pumped into the system by the US Fed.

The repo market blew out in mid-September. It had already briefly blown out at the end of 2018, then settled back down. But the issues started bubbling up again. By the end of July, the repo problems made their way into the Fed’s meeting, as we learned when the minutes of that meeting were released in August.

The repo market is huge. According to the Securities Industry and Financial Markets Association SIFMA, the average daily repos and reverse repos outstanding in 2018 totaled nearly $4 trillion. Repos accounted for $2.2 trillion, reverse repos accounted for $1.7 trillion. The Fed is now playing in both, repos and reverse repos.

So the repo market – with about $2.2 trillion outstanding – blew up in mid-September and repo rates spiked to 10% before the Fed stepped into it to calm it down and keep some financial outfits from blowing up. Perhaps the Fed was fretting about contagion spreading to the rest of the financial system and potentially cause some real damage.

(https://wolfstreet.com/2019/11/06/whats-behind-the-feds-bailout-of-the-repo-market/)

This was only the tip of the iceberg, however, and a sign of deep systemic distress. In its 2019 annual report, the Bank for International Settlements (the central bank of central banks) issued a warning relating to overheating in the leveraged loan markets, in effect maintaining that an equivalent situation to the subprime crisis was once again brewing, with worthless collateralized debt instruments destabilizing global finance.

In early August that same year, the BIS then issues a white paper recommending a radical infusion of credit into the system to prevent a crisis, after which we then had the September repo crisis. The bailout, i.e. the radical infusion of capital into the system, commences the very day after the interest rate spike.

And in October, of course, we have Event 201, and the WHO declaration of the covid pandemic a few months later.

The covid event was an excellent rationale for introducing the centralized interventions designed to address the structural imbalances and coming supply shocks. It provides cover for major capital injections all over the global economy, and immediately and drastically reduced energy consumption in a more or less symmetrical fashion, without the insuperable political unrest and panic which would ensue if spades were called spades here.

The Big Freeze economic theory suggests freezing all time-related fixed expenses – such as rent or mortgage payments, health insurance – and supporting businesses to temporarily close. It provides a Universal Basic Income (UBI) to individuals, together with temporarily increasing marginal taxes for those who haven't been hurt or may even gain from the situation. The goal is to prevent debt, preserve existing economic infrastructure, protect individuals, and position businesses for a smooth market re-entry when the time is right (“COVID-19: How a financial freeze could protect us from economic collapse, World Economic Forum, May 2020).

All of this helped prop up the stock market and probably staved off financial collapse, but it also indirectly provides the framework for the long-term reduction of consumption demanded by supply limits, while leaving property and power relations more or less intact.

In other words, the digitalized control grid now being erected in the wake of the covid event, and which will increasingly be framed in relation to climate change, is their long emergency plan for peak oil. The reduction of consumption by intrusive surveillance and centralized scrutiny over any and all transactions are the building blocks of the new permanent austerity in the embryonic post-modern neofeudalism where your (increasingly rare) children and grandchildren will grow up.

This is of course impossible without the naked authoritarianism increasingly prominent throughout our societies, which is why blaming the Canadian truckers for triggering a cascading chain of events that brings about the next financial crisis is perfectly in line with the overall development of this situation. Since they basically are the supply chain, such blame is almost entirely reasonable at first glance.

In an increasingly precarious situation, actual dissent will be much more intolerable from the system’s point of view. Disciplining and scapegoating dissidents is a natural first step in establishing a more strictly regimented austere West, and it seems inevitable that the coming economic disruptions and food shortages will be blamed on climate change denialism and non-virtuous patterns of consumption rather than the actual underlying scarcities.

What’s the next step? It seems like covid is being called off, replaced by the Red Scare Hate Week and some sabre rattling. There are threats of runaway inflation on the horizon (which effectively empoverishes everyone except the holders of tangible productive assets, i.e. the working class), and there are interesting correlations between the vaccine rollout and a positively immense uptick in a wide variety of severe illnesses.

Living in interesting times indeed.

Great analysis.

I think this analysis is over the target with respect to Hydrocarbons production but plateau oil is a better description or even Plateau hydro carbons. The price of oil and access to oil are of curse key but controlling the medium term price and who has the currency to purchase it is the bigger play in my opinion. Controlling access to energy through carbon credits issued for renewables is a way of enforcing a deflationary Carbon currency standard.

The key ratio is 16:1

https://notthegrubstreetjournal.com/2022/02/06/the-six-ways-on-sunday-carbon-currency-end-game-16-to-1-on-what-are-the-odds-of-that/

https://notthegrubstreetjournal.com/2022/01/10/peak-prometheus-noting-to-see-here-dont-look-up-bruce-charlton-distracted-obiedience-its-got-electrolytes/